I bet many readers are scanning through screeners and news articles trying to find out what the future holds for DraftKings (NASDAQ:DKNG) stock. Well, I’d like you all to remember that if you have a long enough investment horizon, the short-term noise in DKNG stock — or any stock — won’t matter. If you analyze a growth stock based on solid pricing metrics, not even a bearish report by Hindenburg Research will alter its long-term fate.

Upon writing this article, I wanted to convey to investors the actual driving forces behind DraftKings’ stock instead of wasting everybody’s time with subjective thoughts. I hope you all enjoy the read and find my analysis helpful.

Earnings & Guidance for DKNG Stock

DraftKings beat its second-quarter revenue estimates in August. The company reported $298 million in revenue, producing 320.1% in year-over-year growth. Perhaps the key driving factor behind the strong quarter was the 281% year-over-year growth in B2C monthly unique payers. Also worth mentioning is an increase in average revenue per monthly unique payers to $80 (+26% year-over-year).

After its strong quarter, DraftKings raised its revenue outlook for the full year to a range of $1.21 billion – $1.29 billion from its previous estimate of $1.05 billion – $1.15 billion.

Cost of Capital

The sports entertainment and gaming company has managed to lower its cost of capital during the second half of the year. During the first half of 2021, we saw a significant increase in the company’s weighted cost of capital, which could’ve been a contributing factor to the stock’s decline between the months of March to May.

{kind=link}

A reason for the improvement in WACC could be that between January and June, DraftKings managed to decrease its operating expenses, subsequently leveraging its position for better borrowing rates.

A second reason could be a lower return demanded from ordinary shareholders; DraftKings has reduced its Beta from 2.37 to 1.94 over the past year while improving its free cash flow yield from -2.85% a year ago to -1.72%.

If the company can continue producing blockbuster financial results, it will surely continue decreasing its cost of capital, which will bolster the stock’s intrinsic value.

Pricing Factors for DKNG Stocks

Pricing the asset from a growth vantage point, I believed the following factors to be the most important:

- Small-Cap Vs. Large-Cap performance

- Real GDP Outlook

- Value Vs. Growth Performance

{kind=link}

Source: Gurufocus

DraftKings being a large-cap stock at a market cap above $10 billion should continue performing well unless market circumstances change drastically. I personally don’t see investors favoring small-cap stocks again until mid-2022. Small-cap stock performance is very much linked to real economic growth and low inflation.

Goldman Sachs recently upgraded its 2022 real GDP growth estimate from 4.3% to 4.6% but has cut its 2021 GDP estimate for the second time to 5.7% from an initial 6.2%. The Conference Board also cut its fourth-quarter economic growth outlook to 6%, citing slower than anticipated growth in the third quarter as their main reason.

{kind=link}

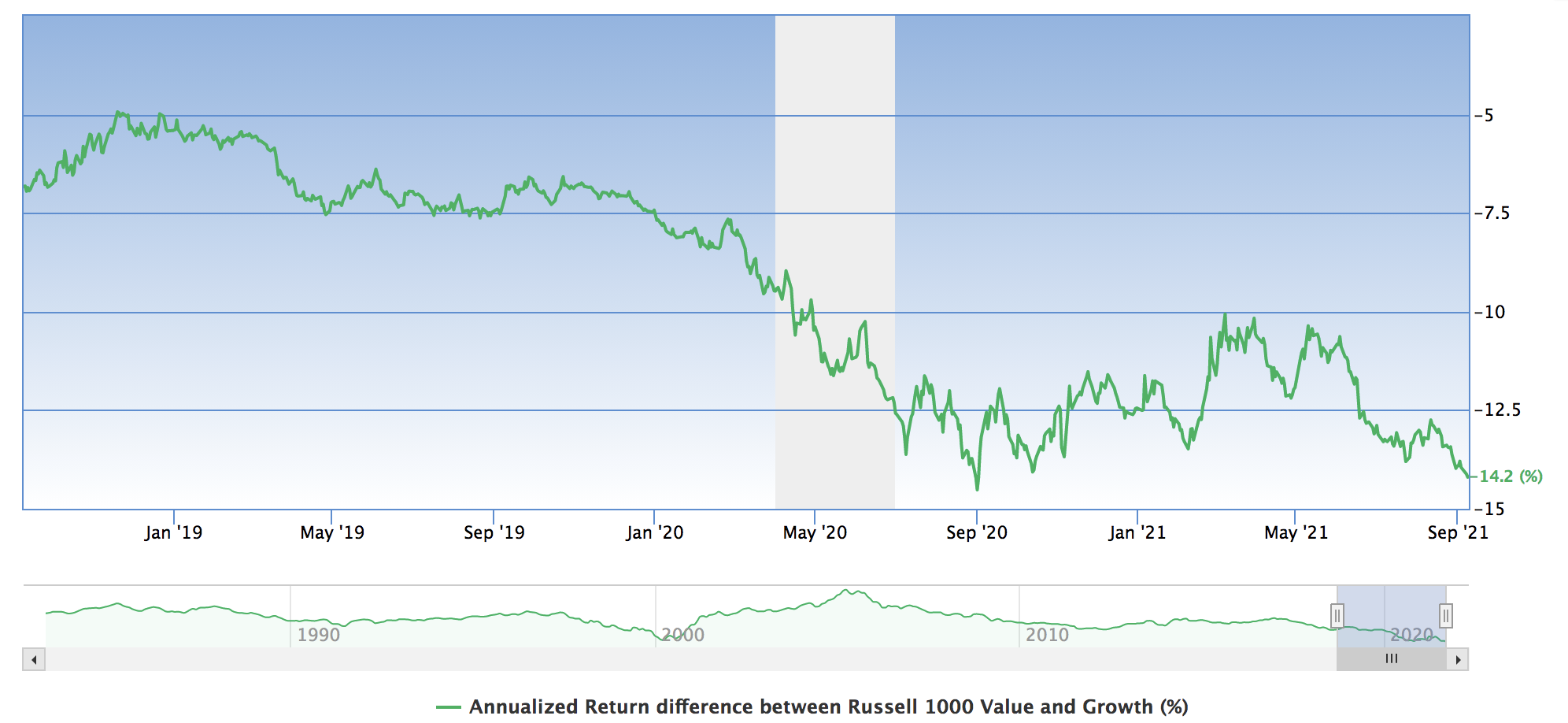

Source: Gurufocus

The chart above illustrates the performance of large-cap value stocks versus large-cap growth stocks.

Value stocks were favored at the start of the year but have been underperforming growth stocks for a significant amount of time.

If the long-term trend had to continue, DraftKings would most likely be an investors’ favorite considering its robust earnings growth and its improved cost of capital.

On the date of publication, Steve Booyens did not hold any long or short positions in any of the securities mentioned. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

Steve Booyens co-founded Pearl Gray Equity and Research in 2020 and has been responsible for equity research and PR ever since. Before founding the firm, Steve spent time working in various finance roles in London and South Africa, and his articles are published on various reputable web pages such as Seeking Alpha, Benzinga, Gurufocus, and Yahoo Finance. Steve’s content for InvestorPlace includes stock recommendations, with occasional articles on crowdfunding, cryptocurrency, and ESG.